Updated Home Equity Conversion Mortgage (HECM) Loan Limits for 2026

The Federal Housing Administration (FHA) has bumped up its maximum claim amount for HECM reverse mortgages this year. The new ceiling is $1,249,125, up from last year’s $1,209,750. Sound like industry jargon? Don’t worry—we’ll break down what this change means for homeowners in plain English below.

Home Equity Conversion Mortgage (HECM) Loan Essentials

HECMs are FHA-insured reverse mortgages available exclusively to homeowners who are at least 62 years old. These loans let you access a portion of your home’s value in flexible ways—as an immediate cash disbursement, ongoing monthly income, a standby line of credit, or a personalized blend of all three options.

What makes HECMs particularly appealing is the payment flexibility they offer. Unlike traditional mortgages, there are no required monthly principal and interest payments. Instead, the loan balance doesn’t need to be repaid until the borrower sells the home, moves out permanently, or passes away. Homeowners simply have to pay their essential property charges, such as taxes, insurance and home maintenance.

Want to dive deeper into how HECMs work? Check out our comprehensive guide: What Is a Reverse Mortgage and How Does it Work?

Understanding HECM Principal Limits

When researching reverse mortgages, “principal limit” is a term you’ll see frequently. It represents the total borrowing capacity available to a qualified homeowner—essentially, the upper boundary of what you can access. The lender applies this principal limit first to satisfy any existing mortgage debt or liens against the home. The balance that remains is your net principal limit, which you’re free to allocate as needed: supplementing retirement income, paying for in-home care, making home repairs, or setting aside for unexpected expenses.

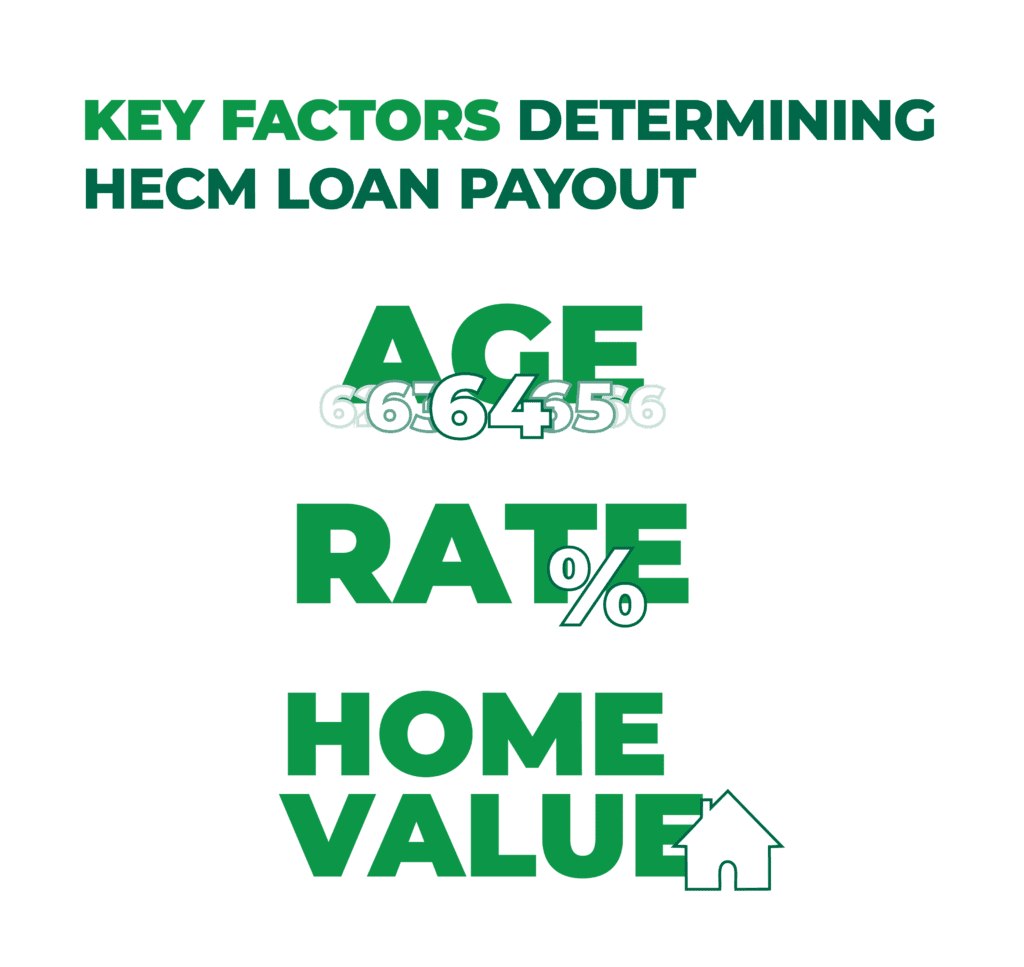

Three Things That Determine Your HECM Loan Amount

Lenders look at three main factors when calculating your initial principal limit:

Your Age (or Your Spouse’s)

If you’re the younger borrower—or if you have a younger eligible non-borrowing spouse—you’ll typically qualify for less money. That’s because the loan will potentially be outstanding for more years.

Current Interest Rate Environment

The expected long-term rate affects how much you can borrow. For adjustable-rate HECMs, this rate is calculated using the 10-year CMT index plus the lender’s margin. Here’s the relationship: higher expected rates mean lower borrowing limits, and lower expected rates mean higher borrowing limits.

What Your Home Is Worth

Lenders take the lower number between your home’s appraised value and the 2026 HECM maximum of $1,249,125. This becomes your maximum claim amount.

Bottom line: Older borrowers with valuable homes in a low-rate environment will see the highest principal limits.

Want a quick estimate of what you might qualify for? Try our HECM loan calculator.

Why a Higher HECM Limit Matters

If you own a higher-value home, the 2026 HECM limit increase is great news. Here’s why: when determining how much you can borrow, lenders always use whichever number is smaller—your home’s appraised value or the HECM maximum. By raising that maximum from $1,209,750 to $1,249,125, homeowners with properties valued well above the limit can now access more equity than they could last year.

Here’s a concrete example. Imagine a 69-year-old homeowner with a property worth $1.6 million, using an expected rate of 6.625% (based on FHA’s standard principal limit factors):

What they could access in 2025: $451,236

What they can access in 2026: $465,923

That’s $14,686 more in borrowing power.

NOTE: This is a hypothetical scenario for demonstration purposes. Any individuals mentioned are fictional.

Whether you’re applying for a new HECM or refinancing an existing one, this higher limit can make a real difference. In some cases, that extra cushion means you won’t need to bring your own money to closing to cover an equity gap—a significant advantage.

Protect Your Loan Amount with a Rate Lock

Don’t leave your HECM proceeds to chance. After applying, locking your expected rate shields you from market volatility that could reduce your borrowing capacity before closing. If rates climb during the processing period, an unlocked rate means less money available to you.

The expected rate lock gives you 120 days of protection starting from your FHA case number assignment. The best part? If rates decrease after locking, you still get the advantage of the lower rate. You’re protected from increases but can still benefit from decreases.

Ready to Explore Your Options?

Thinking about tapping into your home equity through a reverse mortgage? Wondering if the timing is right for your situation? Fairway is here to provide the information and guidance you need to make a confident decision about leveraging one of your most significant retirement resources. Let’s talk—reach out today!