The HECM & H4P Advantage: Why Every SRES Agent Needs These Tools

How the Home Equity Conversion Mortgage for Purchase unlocks dream homes for your senior clients — and bigger opportunities for you

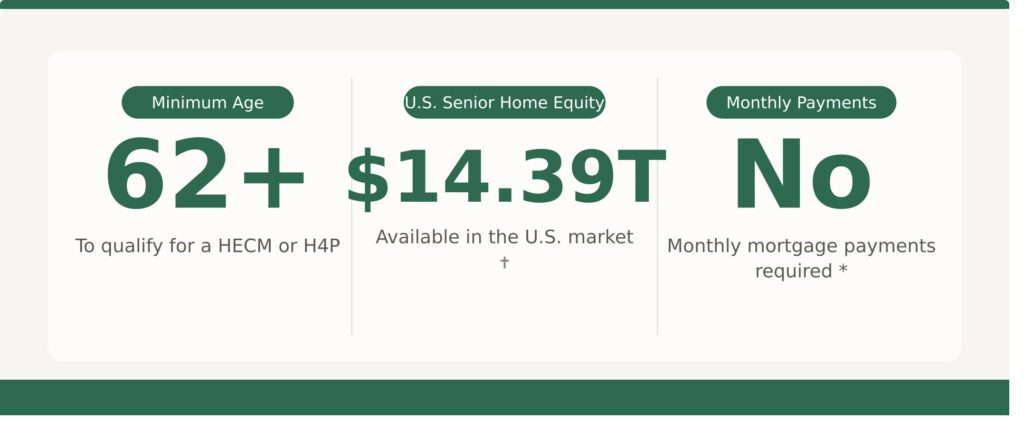

As a realtor with the Seniors Real Estate Specialist (SRES) designation, you understand the unique financial, physical, and emotional landscape of buyers and sellers age 62 and older. This demographic is growing, motivated, and often sitting on decades of accumulated home equity. There’s a powerful financing tool that most SRES professionals haven’t fully integrated into their practice — and once you do, it can transform the way you serve senior clients and grow your business.

It’s called a Home Equity Conversion Mortgage (HECM), and, more specifically for your buyer clients, the HECM for Purchase (H4P).

What Is a HECM, and Why Does It Matter?

The Home Equity Conversion Mortgage (HECM) is the federal government’s reverse mortgage loan program. Insured by the Federal Housing Administration (FHA) and administered under the Department of Housing and Urban Development (HUD), it allows qualified homeowners aged 62 or older to convert a portion of their home equity into usable funds without requiring a monthly mortgage payment. Borrowers remain responsible for property taxes, homeowner’s insurance, and maintenance, but the loan itself doesn’t come due until the last borrower permanently leaves the home.

For homeowners who already own their residence, a HECM can eliminate an existing mortgage payment, create a growing line of credit, fund in-home care, or simply provide financial breathing room in retirement. However, the version that should most excite you as an SRES agent is the HECM for Purchase.

What Is the HECM for Purchase, and Why Does It Matter?

The HECM for Purchase — commonly called the H4P — is a government-insured loan that allows seniors to purchase a new primary residence using a combination of their own funds (typically proceeds from the sale of their current home) and H4P loan proceeds. The result? They move into the home they truly want, preserve a significant portion of their sale proceeds, and carry no monthly mortgage payment going forward, so long as they maintain the home and pay taxes and insurance.

With an H4P, a senior buyer can often purchase a home worth considerably more than they could afford with a conventional mortgage, because monthly payment qualification is not the constraint.

Here’s how it works at a high level: The amount the borrower must bring to closing is determined by their age (or the age of the younger spouse), prevailing interest rates, and the appraised value or purchase price of the new home — whichever is lower. Typically, borrowers need to bring roughly 40%-60% of the home’s value to closing, with the H4P covering the rest. The older the borrower, the more the H4P can contribute, and the less the buyer needs to provide.

How the H4P Opens Doors Seniors Didn’t Know Were Available

Your senior clients often face a frustrating paradox: they have real wealth in the home equity they’ve built over decades, but limited monthly income. When they go to a conventional lender, they’re underqualified. Debt-to-income ratios, monthly payment calculations, and income documentation requirements conspire to cap them at purchase prices far below what they can actually afford in terms of total wealth.

The H4P reframes the entire conversation. Consider these real-world scenarios:

The Downsizer Who Wants to Upsize

A client sells a large family home for $650,000. With a conventional loan, their Social Security income limits them to a $400,000 purchase. With an H4P, they can target a $550,000+ home, preserve $250,000+ in liquid savings, and pay nothing on the mortgage each month so long as they stay current on maintenance, taxes, and insurance.

With a HECM, the borrower has no obligation to make monthly mortgage payments. Instead, they’re responsible for the property charges they already had to pay, such as taxes, insurance, and home upkeep. Interest and loan fees accumulate over time, causing the loan balance to increase. Borrowers may make voluntary payments of any amount, whenever they choose, to control the balance growth or for tax purposes. Repayment isn’t required until the property is sold, the borrower relocates permanently, or passes away. The FHA’s non-recourse protection ensures that neither borrowers nor their heirs will owe more than the home’s value when sold.*

The Retirement Dream Home

A couple has dreamed of a waterfront or golf-community home but assumed it was out of reach on their fixed income. With H4P proceeds boosting their purchasing power and no monthly payment requirement (must pay taxes and insurance), that dream may be fully attainable.

The Accessibility Move

A senior needs to move to a single-floor home or a community with amenities suited to aging in place. An H4P lets them purchase a purpose-built accessible home in the right neighborhood — one they couldn’t otherwise finance on a limited income.

Moving Closer to Family

Clients want to relocate to be near adult children, but homes in that target market are more expensive. The H4P bridges the gap between what their equity provides and what the market requires, without a monthly payment burden, since they only need to cover taxes and insurance.

In each of these cases, the senior gets the home they actually want — not the home their fixed income would otherwise allow. Their quality of life, safety, and well-being all improve. That’s the human core of the H4P, and it’s why you owe it to your clients to understand this loan.

How the H4P Helps Your Business: More Closings, Larger Sales

Now let’s talk about the direct and significant advantages this provides to you as an SRES professional.

Unlock the “Can’t Afford It” Client

How many times has a senior client fallen in love with a property only to see the transaction fall apart when a conventional lender couldn’t qualify them? The H4P can help eliminate that failure point. Clients who walked away from listings they loved can now come back to the table. You don’t lose the sale; you find a solution.

Increase the Price Range (and Your Commissions)

As the H4P amplifies purchasing power, your clients can realistically shop in higher price brackets. A client you might have shown $350,000 listings to could now be a genuine buyer at $500,000 or $600,000. That difference has a direct and meaningful impact on your commission. For SRES agents willing to become fluent in the H4P, this can be transformational over the course of a year’s worth of transactions.

Differentiate Yourself in the Senior Market

The SRES designation already sets you apart. Adding deep expertise in H4P financing makes you genuinely irreplaceable to senior buyers. When adult children are helping their parents navigate a move, and you can walk them through financing solutions that conventional agents don’t even know exist, you become the obvious trusted advisor. The referrals from that kind of expertise compound quickly.

Smoother Transactions With All-Cash-Like Closing Profiles

H4P transactions, once fully underwritten, close with a strong and reliable profile. Unlike conventional financing, there is no traditional income-based approval process, and many of the income-documentation hurdles that typically derail senior buyers simply don’t exist. The transaction moves with greater predictability, and sellers respond well.

How the H4P Helps You Serve Senior Clients Better

- Converts formerly unqualified buyers into active, motivated purchasers

- Expands your clients’ realistic shopping range (often by $100,000–$200,000 or more)

- Preserves your clients’ liquid savings, leaving them financially secure post-closing

- Eliminates the monthly payment burden that often causes hesitation in senior buyers (must pay taxes and insurance)

- Gives you a powerful differentiator in the growing 62+ buyer segment

- Positions you as the go-to agent when financial advisors and elder care professionals refer clients

How the H4P Helps Your Business: More Closings, Larger Sales

Beyond the business case, these loans can meaningfully improve the lives of the people you serve.

Aging in Place on Their Own Terms

The overwhelming majority of seniors say they want to remain in their homes as long as possible. A HECM can make that possible by eliminating an existing mortgage payment (must pay taxes and insurance), freeing up cash flow for in-home care, or funding accessibility modifications like ramps, wider doorways, walk-in showers, and stair lifts. The ability to stay in a familiar home, in a familiar neighborhood, close to friends and community, isn’t trivial. For senior clients, it’s deeply connected to health, cognitive vitality, and emotional well-being.

Financial Security Without Sacrificing Quality of Life

Outliving savings is one of the great anxieties for retirees. A HECM line of credit that grows over time, available but untouched unless needed. It can provide a safety net, allowing seniors to live comfortably, travel, support grandchildren’s education, and handle unexpected medical costs without depleting their investment portfolios in down markets. It provides a kind of financial resilience that planners and advisors now consider a cornerstone of sound retirement strategy.**

The Right Home at the Right Time

With an H4P, a senior doesn’t have to settle. They can purchase the home that suits their physical needs — single-story, accessible, close to medical facilities or family — in the community that will genuinely serve them for the next 20-30 years. It’s an extraordinary gift, and you are in a position to make it happen.

Preserving the Estate

A common misconception is that a reverse mortgage depletes an estate. In reality, when a senior uses an H4P to purchase a home, they own the home, and the title is in their name. Their heirs inherit the property and can sell it, repay the loan balance (which can never exceed the home’s value, thanks to FHA insurance), and keep any remaining equity. In many scenarios, particularly when home values appreciate over time, the H4P is entirely compatible with estate planning goals.**

When a senior client can buy the home they truly want, live there without a monthly mortgage payment,* and preserve their savings for what matters most, that is a genuinely life-changing outcome.

Common Misconceptions and the Actual Facts

Part of your role as an SRES professional is to help clients and their families navigate misinformation. Here are the most common objections you’ll hear and the truth behind them.

“The bank will own my home.”

False. The borrower retains title to their home throughout the life of the loan. The lender holds a lien — just as with any mortgage — but ownership remains with the borrower.

“My heirs will be left with nothing.”

Not accurate in most cases. Thanks to FHA insurance, the loan can never exceed the home’s appraised value at the time of repayment. If the home has appreciated (as most homes in New England have), heirs often receive substantial equity after repaying the loan, and no heir is ever personally liable for a deficiency.

“I’ll be forced to move.”

A HECM or H4P loan doesn’t come due as long as the borrower lives in the home as their primary residence and meets basic obligations, like maintaining the property and staying current on taxes and insurance. There is no scenario in which a lender forces a borrower out as long as the borrower meets those conditions.

Your Partnership With Fairway Reverse Mortgage New England

At Fairway Reverse Mortgage New England, we specialize exclusively in reverse mortgage products — the HECM, H4P, Jumbo Reverse Mortgage, and HomeSafe Second. Our team works daily with real estate professionals throughout Massachusetts and New England to structure H4P transactions that close smoothly and serve seniors well. We provide education, scenario illustrations, and direct support through every step of the process.

We know that the first H4P transaction can feel unfamiliar — the mechanics differ from conventional financing, and your clients may have questions you haven’t encountered before. That’s why we make ourselves available as your resource, not just the lender. We’re happy to join client presentations, explain the product to adult children, and ensure your clients receive the independent HUD-approved counseling required (and genuinely valuable) as part of the H4P process.

If you serve seniors, the H4P belongs in your toolkit. Your clients are out there right now, but they’re constrained by conventional financing limits, settling for homes that don’t truly fit their needs or sitting on the sidelines entirely. Give them a better option and build the kind of practice that the growing senior population in New England deserves.

Ready To Learn More?

Contact us today for a free consultation, scenario illustrations for your clients, or to schedule an SRES-focused presentation for your office.

*Borrower is still responsible for essential property charges, such as taxes, insurance, and maintenance.

**This does not constitute tax or financial advice. Please consult a tax advisor or financial professional regarding your situation.